UPDATE – 13 APRIL 2022

Legislation has been passed to enact the following tax-related measures announced in the budget:

- The tax deductibility of COVID-19 tests for the purposes of attending your workplace or required during the course of carrying on your business;

- The increase to the low and middle income tax offset by $420 (to $1,500);

- A one-off cost of living payment of $250 to certain social security and pension recipients;

- A reduction to the GDP factor for 2022-23 for the calculation of PAYG and GST instalments;

- A 50% reduction to fuel excise and excise-equivalent customs duty;

- The increase in the Medicare Levy low-income thresholds for individuals and families and those eligible for the senior and pensioner tax offset.

Notably, there has not been legislation introduced for the proposed Small Business Skills and Training Boost and the Technology Investment Boost. Given that Parliament has now been dissolved, we will need to await the outcome of the Federal Election to see whether these new measures will be legislated in the future.

On Tuesday night, 29 March 2022, Federal Treasurer Josh Frydenberg handed down his fourth Federal Budget. To be fair, the current Treasurer hasn’t had the easiest of times in the job. Two out of three of his budgets were delivered amidst global pandemic and economic uncertainty. He now faces a ‘make-or-break’ budget with a looming federal election. Pre-budget leaks of direct cash payments and relief at the petrol pump, both targeted at reducing the cost-of-living, turned out to be correct.

Last year, the deficit for the 2021-22 financial year was forecast to be $106.6 billion. This has now improved to $79.8 billion. The improvement seemingly coming from more people back at work and fewer on welfare, meaning the Government has collected more tax revenues than expected.

Key budget measures that will impact on our clients include:

- An extra $420 in individual tax relief for 2022 tax returns (to be lodged from 1 July 2022). This will be reflected in an increase in the low and middle income tax offset (LMITO) to $1,500;

- Temporary full expensing of eligible assets extended to 30 June 2023;

- Temporary reduction to the fuel excise which will reduce fuel costs for individuals and businesses;

- A 120% deduction for eligible costs aimed at encouraging small businesses to adopt digital technologies (like portable payment devices, cyber security systems and subscriptions to cloud-based services); and

- A 120% deduction for costs incurred in training and upskilling staff.

Unfortunately, there was still no substantial debate around the change or movements to GST or significant tax reform. We have an expected late May 2022 Federal election, and a great part of this Budget was aimed at providing immediate relief to taxpayers (rather than addressing any long term, significant tax reform).

We’ve outlined below some of the main tax measures that were announced in the Budget. As with all budgetary measures, these measures are not final until the relevant legislation has been passed by the Government. We will keep you updated on the status of any proposed measures.

Temporary reduction in fuel excise

The excise and excise-equivalent customs duty rate that applies to petrol and diesel will be halved for 6 months (to 28 September 2022).

The current rate of excise and excise-equivalent customs duty is 44.2c/L. This will be halved to 22.1c/L.

The price faced by consumers at the petrol pump is expected to reduce by more than the 22.1c/L given that GST will now be levied on a lower excise amount.

The ACCC will be monitoring the price behaviour of retailers to ensure the lower excise rate is passed on to consumers.

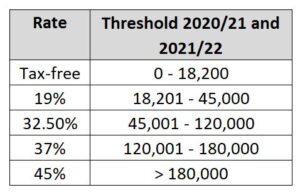

Low and Middle Income Tax Offset

To help ease the increasing costs of living, the Low and Middle Income Tax Offset (LMITO) has been increased. This offset reduces the amount of tax payable by individuals (and will be reflected in a higher tax refund when the 2022 income tax return is lodged).

The LMITO will be increased by $420 for individuals (to $1,500) and by $840 for couples (to $3,000). Taxpayers with incomes of more than $126,000 will not be eligible for the offset.

Cost of living payment

In April, a one-off $250 payment will be made to eligible Australian pensioners, welfare recipients, veterans and concession card holders.

The eligible recipients are those that receive the following payments or hold the relevant concession cards:

- Age pension

- Disability support pension

- Parenting payment

- Carer payment

- Carer allowance

- Jobseeker payment

- Youth Allowance

- Austudy and Abstudy living allowance

- Double orphan pension

- Special benefit

- Farm Household Allowance

- Pensioner Concession Card holders

- Commonwealth Seniors Health Card holders

- Eligible Veterans’ Affairs payment recipients and Veteran Gold Card holders.

The payments are exempt from tax and will not count as income support for the purposes of income support payments. You can only receive one payment (even if you are eligible under 2 or more categories). The payment is only available to Australian residents.

Small Business - Skills and Training Boost

The skills and training boost is designed to support small businesses to train and upskill their employees.

Small businesses (with a turnover of less than $50 million) can claim an additional 20% deduction for expenditure incurred on external training courses provided to their employees.

The external training course must be provided to employees in Australia or online and delivered by entities registered in Australia. It does not include in-house or on-the-job training.

For example, if your business paid $1,000 for your employee to attend a training course, your business could be eligible to claim a deduction of $1,200.

This measure applies to expenditure incurred from 7:30pm, 29 March 2022 to 30 June 2024. Expenditure incurred between 29 March 2022 to 30 June 2022 can only be claimed in the 2023 financial year. Expenditure incurred between 1 July 2022 and 30 June 2024 can be claimed in the year in which it is incurred.

Small Business - Technology Investment Boost

The technology investment boost is designed to encourage digital adoption by small businesses.

Small businesses (with a turnover of less than $50 million) can claim an additional 20% deduction for expenditure incurred on business expenses and depreciating assets that support adoption – for example: portable payment devices, cyber security systems or subscriptions to cloud-based services.

There is a cap of $100,000 on expenditure that will be eligible for the boost.

For example, if your business paid $100 for a subscription to a cloud-based service, your business could be eligible for a deduction of up to $120.

This measure applies to expenditure incurred from 7:30pm, 29 March 2022 to 30 June 2024. Expenditure incurred between 29 March 2022 to 30 June 2022 can only be claimed in the 2023 financial year. Expenditure incurred between 1 July 2022 and 30 June 2024 can be claimed in the year in which it is incurred.

COVID-19 Measures

Business grants

Certain COVID-19 business support program payments (from states and territories) will be non-assessable and non-exempt income until 30 June 2022 (this measure was originally announced on 13 September 2020).

Deductibility of COVID-19 tests

The cost of taking a COVID-19 test to attend a place of work will be tax deductible from 1 July 2021.

Further, fringe benefits tax will not be incurred by businesses where COVID-19 tests are provided to employees for this purpose.

Free Rapid Antigen Tests

The Government will be delivering up to 20 free Rapid Antigen tests to all Australians with a concession card.

Changes to PAYG instalment system

PAYG instalment rates

The GDP uplift factor for PAYG and GST instalments is to be reduced to 2% (currently the statutory rate is 10%). This measure will provide cash flow support to small businesses (including sole traders) and other individuals with investment income.

While this may free up cash in the short term for taxpayers, it is simply deferring the tax liability which may present additional cashflow problems when the end of year tax returns are prepared and final tax liabilities become payable.

Modernisation of PAYG instalment system

It is anticipated that from 1 January 2024, companies can choose to have their PAYG tax instalments calculated based on current financial performance extracted from their business accounting software (with some tax adjustments). This is subject to software providers having the anticipated systems in place by 31 December 2023.

Superannuation - Minimum pension drawdowns

The 50% reduction to minimum pension drawdowns has been extended to 30 June 2023. This will allow retirees to avoid selling down assets in order to have sufficient cashflow to meet the minimum drawdown requirements.

Other measures of interest

Some other measures of interest from a tax perspective include:

- Dad and Partner Pay and Parental Leave pay to be combined into a single scheme with up to 20 weeks, fully flexible and shareable leave available for eligible working parents to take as they see fit. It can be taken at any time within 2 years of the birth or adoption of their child.

- ATO to share STP data with State and Territory Revenue offices on an ongoing basis. This will be used for prefilling of payroll tax returns.

- $80 million in additional support for small and medium export businesses to re-establish their presence in overseas markets through the Export Market Development Grant (EMDG) program.

- Approx. $157 million in assistance to Ukraine (including $91 million in military assistance and $65 million in humanitarian assistance).

- Option to report Taxable Payments Reporting System Data to the ATO on the same lodgement program as activity statements from 1 January 2024. This is subject to the software providers being able to deliver appropriate software by 31 December 2023.

We will keep you up-to-date with the progress of the implementation of these Budget measures.

If you would like to discuss the tax implications of the budget proposals, please call us on (07) 56656469.

DISCLAIMER: The information in this article is general in nature and is not a substitute for professional advice. Accordingly, neither TJN Accountants nor any member or employee of TJN Accountants accepts any responsibility for any loss, however caused, as a result of reliance on this general information. We recommend that our formal advice be sought before acting in any of the areas. The article is issued as a helpful guide to clients and for their private information. Therefore it should be regarded as confidential and not be made available to any person without our consent.

Jeanette has over 20 years experience as an accountant in public practice. She is a Chartered Accountant, registered tax agent and accredited SMSF Association advisor. When she is not helping business owners grow their empires, you will likely find her out running on the trails or at the gym. Book in to see Jeanette today.