On Tuesday night, 12 May 2026, Federal Treasurer Jim Chalmers handed down his fifth Federal Budget for the Labor Government. This year’s Budget proposes significant and unprecedented changes to a number of key taxation areas, including capital gains tax, negative gearing and the taxation of family trusts. If these measures are implemented as proposed, they will represent a substantial shift in taxation policy.

Outlined below are some of the key budget initiatives that may directly impact our clients. As with all budgetary measures, these measures are not final until the relevant legislation has been passed by the Government. We will keep you updated on the status of any proposed measures.

Impact for individuals

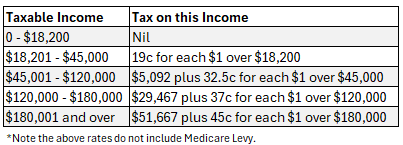

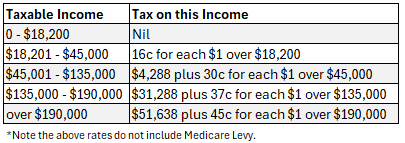

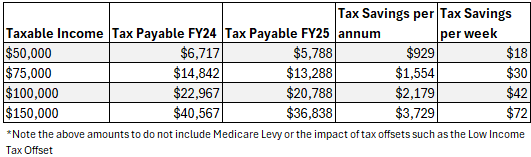

Cuts to individual tax rates (announced in previous budgets)

- From 1 July 2026, the 16% marginal tax rate (for income between $18,201 – $45,000) will drop to 15%, and then to 14% from 1 July 2027.

$250 Working Australians Tax Offset (WATO)

- From 1 July 2027, there will be a permanent tax offset for all Australians who derive income from wages and salary or business income as a sole trader. This will increase the effective tax-free threshold to $24,985 for individuals who are also eligible to the low-income tax offset.

$1,000 instant tax deduction

-

From 1 July 2026, individual taxpayers can claim a $1,000 instant tax deduction for work-related expenses (without the need to keep records). If you have more than $1,000 to claim, the normal deductibility/substantiation rules will apply. You can still claim the following costs (in addition to the $1,000): charitable donations, union fees, professional association membership fees, non-work-related deductions.

Medicare levy

-

Low-income thresholds for Medicare Levy are increasing.

Capital Gains Tax Changes

There are significant changes to capital gains tax (CGT) announced as part of this budget. We will outline the broad impact of these changes as detailed in the budget papers (noting that the draft legislation will provide more detail on how the calculations will be performed):

-

From 1 July 2027, the 50% CGT discount will be replaced by an cost base indexation for assets held for more than 12 months, with a minimum 30% tax on net capital gains.

-

This will apply to all assets, including pre-CGT assets, held by individuals, trusts and companies (although the main residence exemption may still be applicable to the of principal places of residence held by an individual). (Note, there is no mention of changes to CGT calculations for superannuation funds who currently receive a 33% discount for capital assets held for more than 12 months.)

-

Transitional arrangements will ensure that the changes only apply to gains arising on or after 1 July 2027 (such that the discount will be available up to 1 July 2027 and indexation applicable thereafter).

-

To encourage investment in new residential properties, investors will hold new residential properties be able to choose between the 50% discount and the indexed cost base and 30% minimum tax.

Who is impacted: Taxpayers (individuals, trusts and companies) with any capital investments.

Negative Gearing Tax Changes – Residential Rental Properties

There are significant changes to negative gearing for residential rental properties announced as part of this budget. We will outline the broad impact of these changes as detailed in the budget papers (noting that the draft legislation will provide more detail on how the new measures will be implemented):

-

From 1 July 2027, the tax benefits of negative gearing on residential rental properties will only be available for new residential properties.

-

Existing arrangements will remain unchanged for all properties held on or before 12 May 2026 (Budget Night). Properties currently under contract but not yet settled will also be exempt from these changes.

-

Investors investing in established residential houses after 12 May 2026 will not be able to claim the immediate tax benefit of any negative gearing of that property after 1 July 2027. However, any losses incurred on the property can be carried forward and offset against any future income from the property (ie. if it becomes positively geared in the future) or against any future capital gain on the property.

-

It is not proposed that these changes will extend to commercial properties. Nor does it appear that they will extend to investments in shares or other asset classes. It also doesn’t extent to investments held by widely held trusts and superannuation funds. Based on this, you can claim a tax benefit for any negative gearing into commercial rental properties or shares. Also based on this, existing LRBA arrangements that result in negative gearing in superannuation funds for residential property investments, are unlikely to be affected.

Who is impacted: Taxpayers (individual, trust or company) looking to purchase a negatively geared existing residential investment property after 12 May 2026.

Discretionary Trusts – 30% minimum tax

There are significant changes to the taxation of trusts announced as part of this budget. We will outline the broad impact of these changes as detailed in the budget papers (noting that the draft legislation will provide more detail on how it will be implemented):

-

From 1 July 2028, there will be a 30% minimum tax on the taxable income of discretionary trusts.

-

When the income is distributed to beneficiaries, they will receive a non-refundable credit for the tax payable by the trustee (except corporate beneficiaries). Corporate beneficiaries will not receive a credit for the tax paid by the trustee.

-

This will not apply to: fixed trusts, widely held trusts, fixed testamentary trusts, complying superannuation funds, special disability trusts, deceased estates and charitable trusts.

-

This will also not apply to some types of income: primary production income, income relating to vulnerable minors, amounts to which non-resident withholding tax applies, income from assets of a discretionary testamentary trust that existed as at 12 May 2026.

-

There will be rollover relief for three years from 1 July 2027 to support small businesses and others that want to restructure out of discretionary trusts to another structure (like a company or fixed trust).

Who is impacted: All discretionary trusts.

Our comments:

-

Under these proposed measures, distributions to corporate beneficiaries will incur a double layer of tax – 30% paid by the trustee and a further 25%/30% by the corporate beneficiary with no credit for the 30% paid by the trustee. By the time the tax reaches the hands of an individual, the effective tax rate (if distributed via a corporate beneficiary) could be as high as 77%.

-

While the Federal Government is promising “rollover relief” for restructures – there is also a significant possibility of a transfer/stamp duty cost at the state level. This will need to be considered on a state-by-state basis depending on where your business operates or where your investments are held. The Federal Government does not have the power to legislate to exempt a restructure from state-based taxes.

-

If you provide for the establishment of a testamentary trust as part of your estate planning, you should review this with your lawyer and tax adviser to determine if this is still an appropriate strategy for your estate.

Loss Carry-Back

The loss carry-back provisions are also set to return:

-

From 1 July 2026, eligible companies that make a loss in the current income year, can use that loss to get a refund of tax paid in the prior 2 income years.

-

To be eligible, the company needs to have annual global turnover of less than $1 billion.

Our comments:

-

We welcome the return of the loss carry-back provisions especially to support businesses who have a suffered a temporary set-back with their business.

Startup Loss Refunds

From 1 July 2028, startups with an aggregated turnover of less than $10 million may be eligible for a refundable tax offset for their losses. in the first 2 years of operations (limited to the value of fringe benefits tax and withholding tax paid on employee wages).

$20k Instant Asset Write-Off – Permanent

A measure that has been temporary and varied significantly over the past 6 or so years, this Budget will make the Instant Asset Write-Off a permanent part of the legislation.

From 1 July 2026, small businesses with a turnover of up to $10 million will be able to permanently access the instant asset write-off for assets acquired for less than $20,000.

Assets acquired for $20,000 or more can continue to be placed in the simplified depreciation pool and depreciated over time.

Electric Cars & FBT

All electric cars will retain the FBT discount rate that was in place when the arrangement commenced (so all electric cars valued up to and including $75,000 that are provided before 1 April 2029 will continue to be exempt from FBT).

Electric cars that are valued above $75,000 and up to and including the fuel-efficient luxury car threshold that are provided to employees for private use between 1 April 2027 and 1 April 2029 will only be eligible for a 25% discount on FBT.

PAYG instalments

From 1 July 2027, businesses can opt in to monthly PAYG income tax instalments. There is also the option to use ATO-approved calculations imbedded in your accounting software to calculate and vary your instalments. This will help businesses to match their instalments to their business activity.

Taxpayers with a demonstrated history of non-compliance will be required to report and pay PAYG income tax instalments monthly.

We will keep you up-to-date with the progress of the implementation of these Budget measures.

If you would like to discuss the tax implications of the budget proposals, please call us on (07) 56656469.

DISCLAIMER: The information in this article is general in nature and is not a substitute for professional advice. Accordingly, neither TJN Accountants nor any member or employee of TJN Accountants accepts any responsibility for any loss, however caused, as a result of reliance on this general information. We recommend that our formal advice be sought before acting in any of the areas. The article is issued as a helpful guide to clients and for their private information. Therefore it should be regarded as confidential and not be made available to any person without our consent.

Jeanette has over 20 years experience as an accountant in public practice. She is a Chartered Accountant, registered tax agent and accredited SMSF Association advisor. When she is not helping business owners grow their empires, you will likely find her out running on the trails or at the gym. Book in to see Jeanette today.